A Better Way to Manage Your Household Finances

Meet Frank, a powerful personal finance tool that brings your accounts, goals, and decisions into one clear, easy-to-manage system. Built for busy people with busy lives, Frank helps you stay on top of your money without obsessing over every detail.

Less financial stress. More confident decisions.

What You Get With Frank

Frank isn’t just another budgeting app or financial dashboard. He’s also your personal advisor, powered by our proprietary AI engine, and an expert on all things finance.

Connect your accounts and see your finances in a single view. Frank pulls your financial life together so you don’t have to juggle logins, spreadsheets, or half-remembered balances.

You never need to nod along while someone talks over your head. You choose how Frank looks, sounds, and explains things, because truly good advice is easy to understand and comes from someone you trust.

No need to obsessively check your accounts. Frank’s got your back. He keeps an eye on your finances and alerts you if something seems off, whether it’s a spending shift, a missed opportunity, or a potential issue.

Life has a way of throwing curveballs. Should you finance a new HVAC system you need but can’t afford? Is it more important to exercise stock options or pay down the credit card? Frank is available to chat 24/7 with answers grounded in your real financial picture, so you don’t have to guess or go it alone.

Things may come up that you’d prefer to hash out with a person. A subscription includes two 60-minute planning sessions each year with a CFP® professional to dig into specific questions or your overall trajectory and long-term plan.

How It Works

Simple, fast, and customized.

.png)

Get Frank's Take

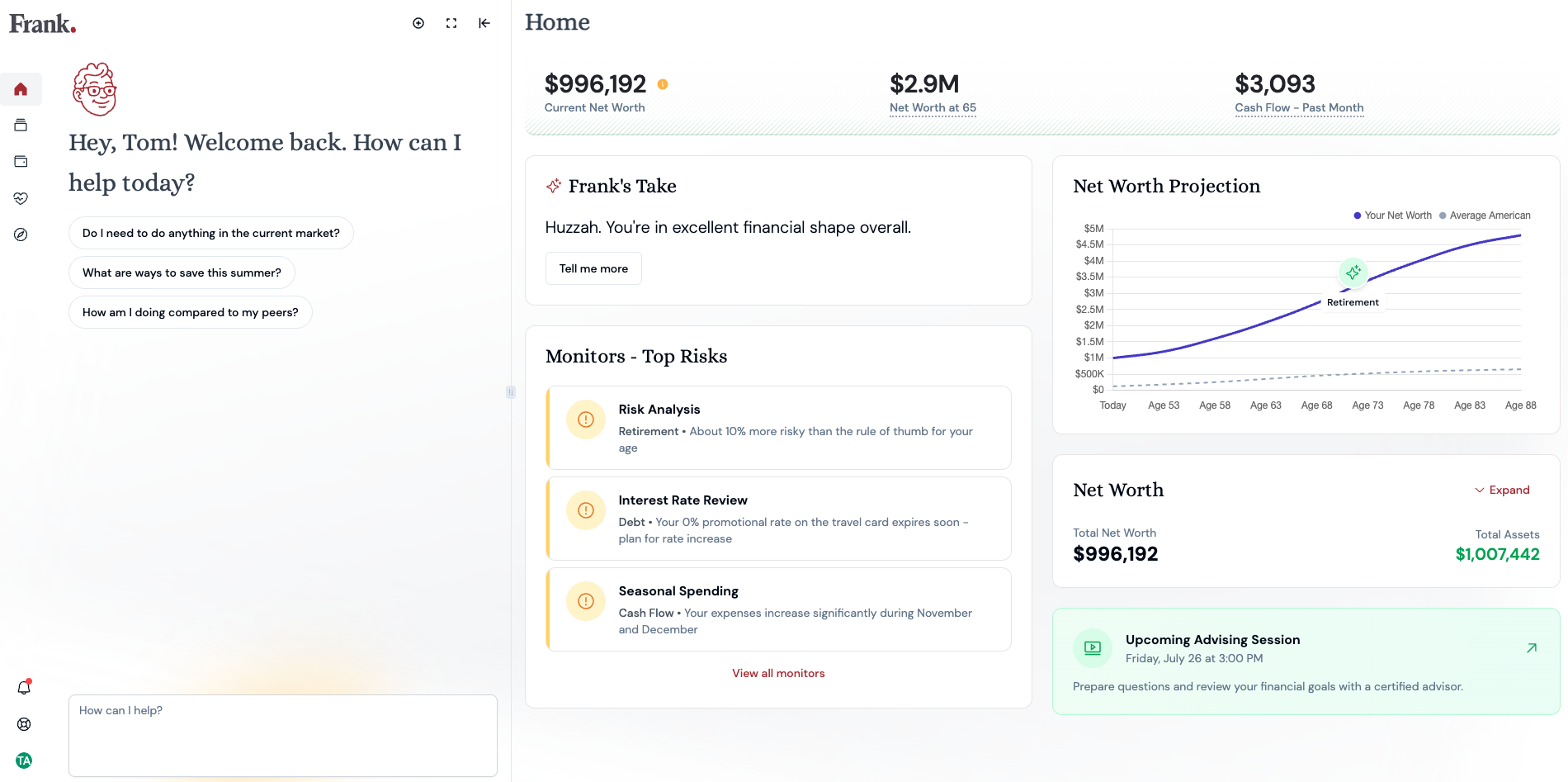

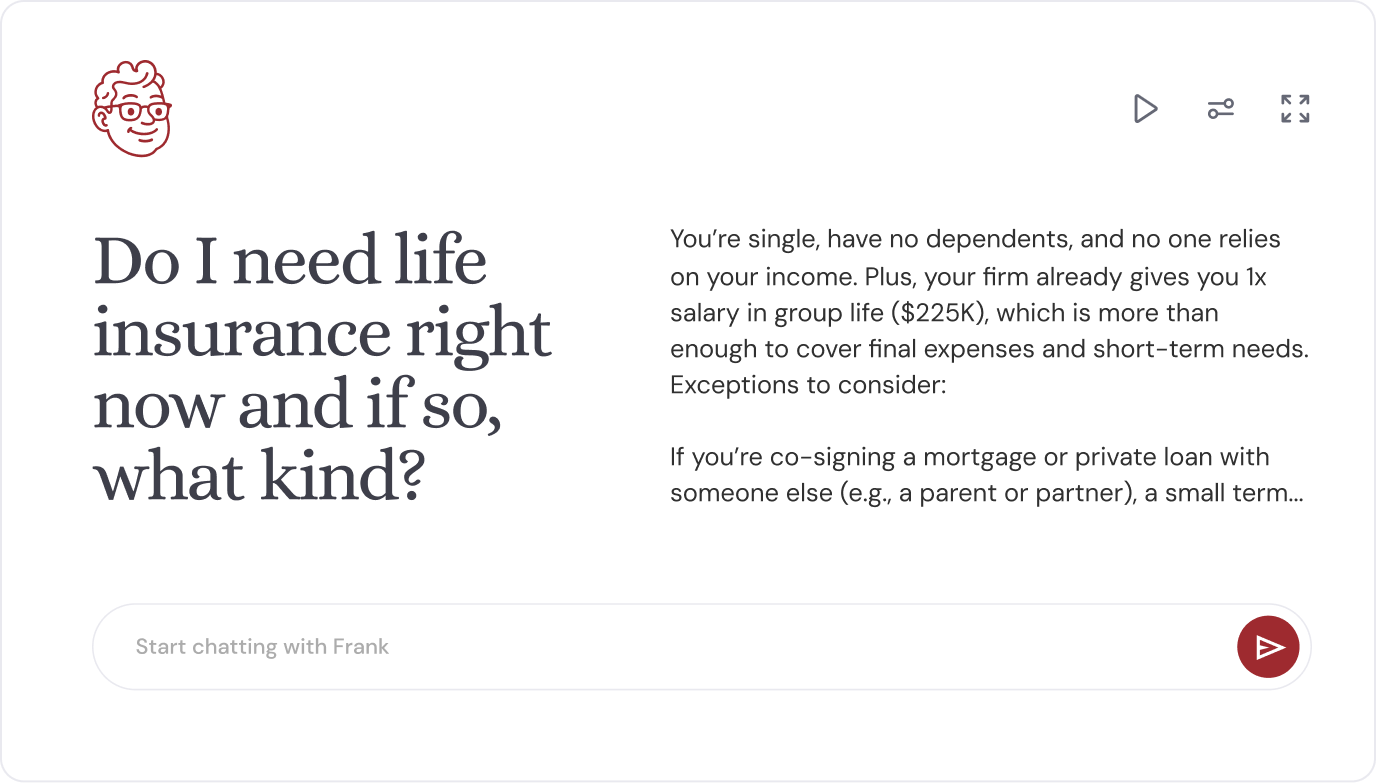

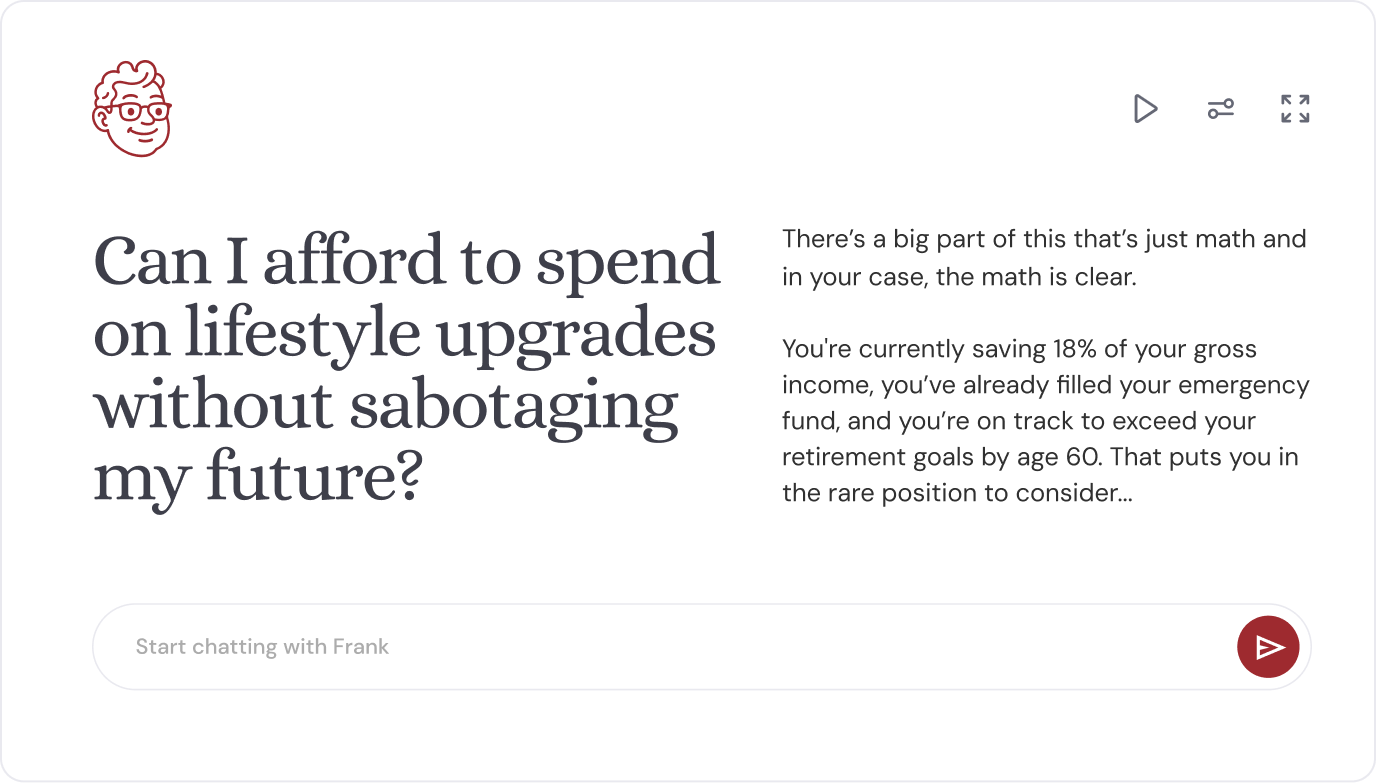

Frank’s purpose-built chat experience is designed to do more than just answer questions. He listens and learns, guiding you step-by-step through practical financial decisions.

And if you ever want a second opinion? A human advisor is just a tap away.

Why People Turn to Frank

Frank is built for people who already manage their money well but want added confidence and thoughtful guidance for financial decisions. If any of these sound familiar, you’re in the right place.

A financial advisor who gets you. Finally.

Need Peace of Mind? Get Frank.

Frank was built to simplify your financial life and streamline your decisions. No need to obsess over market updates or spend your time poring over spreadsheets. Frank will give you the bottom line on financial decisions, so you’re free to focus on what matters.